(1).bmp)

Internal devaluation: nothing but sweat and tears?

The Lettre du CEPII No. 324 shows that internal devaluation strategies in Latvia and in Ireland produced only limited adjustments at the price of considerable social costs.

Par Sophie Piton, Yves-Emmanuel Bara

The concept of internal devaluation was first coined at the beginning of the 1990’s, when Finland and Sweden were considering the opportunity of joining the euro. Within a fixed exchange-rate regime –like currency boards or monetary unions- current-account disequilibria adjustment can no longer be carried out through exchange-rate variation: direct action on prices is needed. Internal devaluation strategies consist in deflationary policies aimed at decreasing production costs and the implementation of structural reforms. In practice however, governments have no influence on overall prices and must rely on the propagation of a substantial cut in civil servants’ wages to the private sector’s salaries, and eventually to producer prices. The process should lead to a shift in investment from the non-tradable towards the tradable sector. Structural reforms should allow for increased productivity.

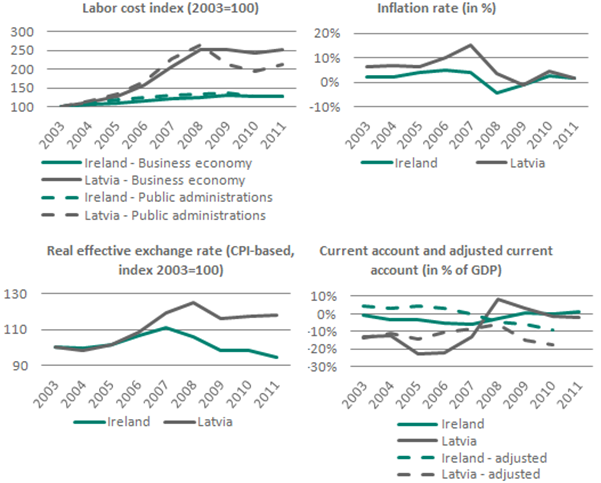

Ireland and Latvia were branded as “role models” by the European Commission because they followed such a strategy in tackling their own imbalances since 2008. These « internal devaluation » processes are however controversial: if some hailed Latvia for its alleged recovery [1], several authors raised serious doubts about its reach and pointed at the social costs of the implemented policies [2].

Substantial cuts in public servants wages (by 4.4% in 2010 in Ireland, by 13.2% in 2009 and 8.1% in 2010 in Latvia) and the reductions in public service payroll (a 19% cut between 2008 and 2010 in Latvia) had only limited impacts on private sector wages and prices. Consumer prices fell by only 2.1% in Ireland between 2008 and 2011 while prices increased by a whopping 6% in Latvia over the same period. Both countries’ real effective exchange rates have only moderately depreciated: by 11% in Ireland and 7% in Latvia. Latvia’s current account showed a surplus in 2009 but, as early as 2011, returned to negative grounds. These adjustments are not sustainable as they mainly rest on domestic demand collapse and not on competitiveness improvements: adjusted for domestic demand fluctuations [3], the current account deficit in Latvia would reach 6% of GDP in 2009 and 18% in 2011.

Ireland and Latvia were branded as “role models” by the European Commission because they followed such a strategy in tackling their own imbalances since 2008. These « internal devaluation » processes are however controversial: if some hailed Latvia for its alleged recovery [1], several authors raised serious doubts about its reach and pointed at the social costs of the implemented policies [2].

Substantial cuts in public servants wages (by 4.4% in 2010 in Ireland, by 13.2% in 2009 and 8.1% in 2010 in Latvia) and the reductions in public service payroll (a 19% cut between 2008 and 2010 in Latvia) had only limited impacts on private sector wages and prices. Consumer prices fell by only 2.1% in Ireland between 2008 and 2011 while prices increased by a whopping 6% in Latvia over the same period. Both countries’ real effective exchange rates have only moderately depreciated: by 11% in Ireland and 7% in Latvia. Latvia’s current account showed a surplus in 2009 but, as early as 2011, returned to negative grounds. These adjustments are not sustainable as they mainly rest on domestic demand collapse and not on competitiveness improvements: adjusted for domestic demand fluctuations [3], the current account deficit in Latvia would reach 6% of GDP in 2009 and 18% in 2011.

These pro-cyclical policies have exacerbated an already difficult situation: Ireland and Latvia were stuck in a deep recession from 2008 to 2010, with GDP contracting by respectively 10.4% and 21.3% and unemployment substantially rising (by 11 percentage points in Latvia and 7 percentage points in Ireland between 2008 and 2010). These movements will induce significant costs in terms of human capital and social transfers on the long-run. Besides, internal devaluation weighs heavily on the countries’ total debt. In a context of rising public debt due to banking systems rescues, a drop in households’ purchasing power mechanically reduces tax revenue and increases social transfers. Deflation and recession do not allow for private sector deleveraging. This debt overhang is likely to be detrimental to future growth.

Overall, internal devaluation produced in these countries limited results at the cost of widespread social hardship and long-standing strains on domestic demand. Real exchange rate misalignments were wider in Portugal and Greece in 2011 than they were in Ireland and Latvia in 2008. Deflationary policies seem likely to fail in these countries and in any case will not be enough to efficiently curb existing disequilibria. Moreover, deflation could weigh the debt burden down, pushing already high public debt further on an unsustainable trajectory.

Crisis-time adjustment in a monetary union requires collective monitoring; it cannot be unilaterally handled at the national level. Internal devaluation in the periphery must come along higher inflation in the surplus countries in order to ease relative prices adjustment [see La Lettre du CEPII n°319]. Public and household debt restructuring will probably be necessary in order to carry these processes out: excessive curbs on domestic demand coupled with long-lasting austerity could turn rebalancing efforts into depressionary strategies. Eventually, EU structural funds should massively support the periphery's tradable sectors development in order to ensure the adjustment's sustainability.

BARA Y.E. & PITON S. (2012) “Internal vs. External devaluation”, La Lettre du CEPII n°324, August.

[1] For example Aslund A (2011), How Latvia Came Through the Financial Crisis, Peterson Institute for International Economics, 207 pp. et Asmussen J. (2012), “Lessons from Latvia and the Baltics”, introductory remarks, Riga, disponible sur le site internet de la BCE (http://www.ecb.int).

[2] For example Rodrik D. (2012), “What I learned in Latvia“, Dani Rodrik’s weblog, http://rodrik.typepad.com ou Krugman P. (2012), “Latvian competitiveness“, The conscience of a liberal, http://krugman.blogs.nytimes.com.

[3] To obtain the current account adjusted for domestic demand fluctuations, we extract from the current balance imports variations related to domestic demand changes. To calculate these variations, we adjust imports for domestic demand fluctuations using an elasticity of imports to final demand of 1.5, in line with the literature.

|

Retrouvez plus d'information sur le blog du CEPII. © CEPII, Reproduction strictement interdite. Le blog du CEPII, ISSN: 2270-2571 |

|||

|